The first wave of pre-2020 lease expirations has cleared. Most portfolios extended, bridged, or renewed under uncertainty and moved on. What's left is the tail, and it's disproportionately high-stakes.

These are the bigger leases. The higher-cost markets. The headquarters and anchor locations that defined the portfolio before the workforce moved. They're coming due in a market that has structurally changed, for a workforce that has too, with more data available to inform the decision than most CRE leaders are using.

The demand pattern has shifted. The portfolio hasn't.

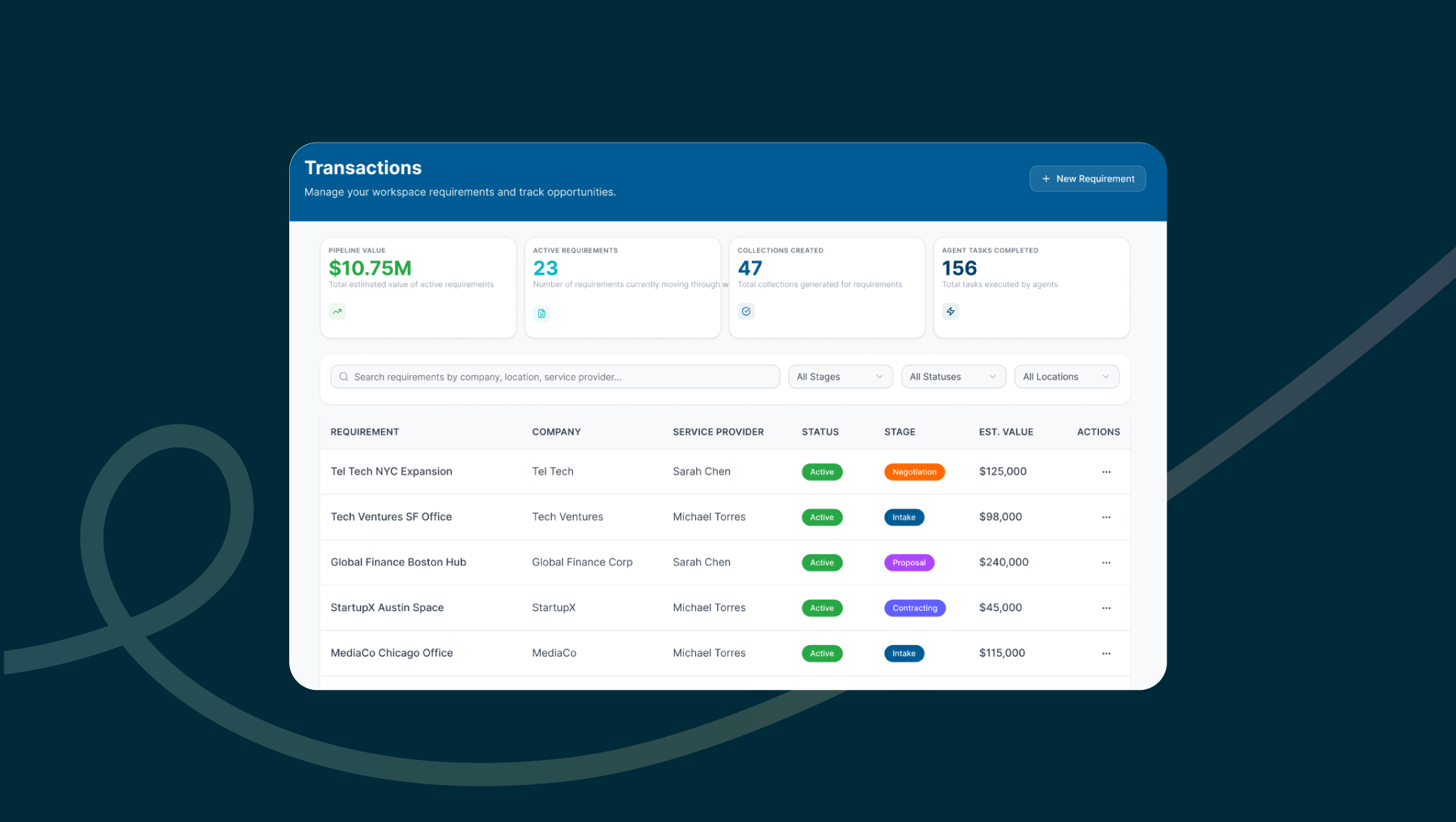

The clearest signal in our platform data is how enterprises are using flexible office differently than they were six years ago.

Before 2020, month-to-month commitments accounted for just over half of all dedicated office bookings on our platform. The remaining half was split across shorter and longer terms, with 12-month-plus commitments representing about one in eight transactions.

Since 2022, the ratio of month-to-month has held. What's changed is in the middle: sub-12-month commitments of two to six months have grown as a share of transactions, from roughly one in four to one in three. Companies aren't locking in. They're taking shorter, renewable terms as a deliberate holding position while they figure out what the right fixed-portfolio answer looks like. Flexible space used to be the overflow valve. Now it's how companies buy time while they sort out what comes next.

What that space is being used for has changed just as meaningfully. In the US enterprise market since 2023, coworking accounts for 40% of all on-demand bookings on our platform. Private meeting rooms are 34%. Private offices are 15%.

The dominant use of flexible space right now isn't desk replacement. It's gathering and proximity. Employees are booking space to be near colleagues, not to fill assigned seats in a building the company signed for years ago. That's a structurally different demand signal than what most portfolios were sized to serve in 2019.

The leases coming due were sized for the old signal.

Renewal is an asset. Most portfolios treat it as a deadline.

These leases were committed when full-time attendance was the operating assumption, not the exception. Portfolio locations were chosen before distributed hiring reshaped where employees live. Square footage was set before the workforce demonstrated it would use home and 3rd spaces when given the choice.

And yet the default, when the lease comes due, is renewal. The pressure of continuity wins. The cost of that default compounds quietly, year after year, in space that's funded by a version of work that already stopped existing.

Renewal is the only moment in the real estate cycle when enterprise tenants hold real leverage. Every other moment, the commitment is already in place. Before the lease expires, the tenant controls the conversation. The question is whether that leverage gets used or forfeited by inertia.

T-Mobile used it. They eliminated fixed offices that were seeing minimal utilization and replaced that coverage with flexible access across hundreds of locations in the same markets. Eighty percent cost savings. The portfolio didn't shrink in coverage. It got a whole heckuva lot more honest about what the business actually needed.

Allstate used it. They cut real estate costs from $380 million a year to $130 million — not by reducing coverage, but by replacing fixed commitments that no longer matched how their workforce was actually working. The data informed the decision. The decision matched reality.

This used to be a gut call. Now it's a data question.

Three or four years ago, these decisions got made on broker estimates and spreadsheets built on assumptions. Comprehensive flexible office cost and availability data was thin. Aggregate behavioral data from actual employee choices didn't exist. Scenario modeling was more art than analysis.

That's changed. Where employees are choosing to work when given options is now measurable. What on-demand booking activity looks like in a given market, what it costs, what coverage it provides, is now quantifiable. The question of what happens if you let a lease expire and replace it with flexible capacity in the same market is now answerable before you make the commitment, not after.

In the US enterprise market since 2023, coworking accounts for 40% of all on-demand bookings on our platform. Private meeting rooms are 34%. Private offices are 15%. The dominant use case isn't desk replacement. It's gathering and proximity — employees booking space to be near colleagues, not to fill assigned seats in a building the company signed for years ago. That's a structurally different demand signal than what most portfolios were sized to serve in 2019.

The portfolios that don't use it will keep paying for assumptions nobody stress-tested since 2019. That cost doesn't announce itself. It just compounds.

The data informed the decision. The decision matched reality. That's what this renewal window makes possible. The only question is whether it gets treated that way.